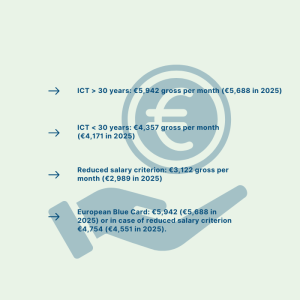

2 November 2023, The Netherlands – Do you have employees that currently benefit from the 30% tax ruling? Then this article cannot be missed moving forward with the implementation of the ruling!

After the announcement earlier this year about the cap off rate for high income earners benefiting from the 30% ruling, the House of Representatives unexpectedly passed two additional amendments to the 30% ruling on 26-27 October. While these two amendments will still have to be approved by the Senate on 19th of December, they already make quite a stir as this would have an impact on the payroll administration. Below you can find an overview of the changes to the 30% ruling announced in 2023:

Per 1st of January 2024:

First amendment

The first amendment will gradually lower the tax free reimbursement from 30% in the first max. 20 months, to 20% in the next max. 20 months, to 10% in the last max. 20 months. After the 60 months, or 5 years, the ruling will come to its end.

This will be applicable to cases that have a 30% ruling approval letter with employment start date of 1st of January 2024 onwards.

Employees who already have the 30% ruling in December 2023 and stay with the same employer will benefit from a transitional arrangement and employees will not be confronted with the cuts until 2026.

Employees who already have the 30% ruling in December 2023 and who will change employer usually will have to reapply for the new ruling. Just like with the amendment passed in 2019 and the transitional arrangement at that time, it is likely that the employee will lose the transitional arrangement and the new measure will also apply to them starting with the new employment as of 1 January 2024.

For employees that currently hold a 30% ruling approval with a duration that is shorter than 60 months, the implementation of the percentage decrease is not yet confirmed by the government. Nevertheless, it has been confirmed that the duration of existing rulings will not be shortened by this amendment.

How this would impact the following situation is not yet known:

- Whether the employer can choose to change to covering the extraterritorial costs on a non-taxed basis instead after receiving the 30% ruling approval, in case the benefit of such is higher after this shift.

Second amendment

The second amendment is that the foreign partial taxation exemption will no longer be applicable starting 2025. This means that it’s no longer possible to opt to be treated as a non-resident for box 2 and 3 and their foreign assets will be private assets and thus taxed as well.

Employees with existing 30% ruling as from December 2023 will be confronted with the abolition from 2027. Again, if employees change employers before this year and do not work consecutively for the new employer, the partial foreign tax liability applies until the change of employers.

Per 1st of January 2023:

The 30% ruling will be capped from 1 January 2024 to the maximum income set by the law “Wet Normering Topinkomens”. This law caps government and non-profit salaries to a maximum amount. For 2023 this cap of amount is 223.000 and for 2024 this will be 233.000 EUR.

Instead of the 30% ruling facility, employers and employees also have to choose whether they want to apply for the 30% ruling or to set up an arrangement in which the employer covers the extra territorial costs. This decision has to be made within the first 4 months of payrolling. With the new amendment, this might be an option that is more beneficial.

Moving forward, to avoid having to gradually lower the percentage of the benefit per 20 months, it is advised to hire new employees at the latest by the 31st of December, rather than the 1st of January.

More details concerning these amendments are expected to be known by December 19th, 2023. We will keep you posted in case of any further updates!

If you are interested in support with the 30% tax ruling or have some questions, feel free to contact us or call us at the phone number +31 (0) 85 – 620 4900.

By Lindy Wentzel, Immigration & Relocation Consultant at PIRGROUP The Netherlands